7 Apr 2022 MAS announced it has transferred to the government S$75B excess OFR (Official Foreign Reserves). These are OFR in excess of their monetary policy management requirements. As a central bank, MAS do not undertake long term and risky investments. The government places these with the sovereign wealth fund GIC for long term investments with better yields.

As usual, such an event is followed by public outcry why with so much reserves, the government is reluctant to increase social spending and instead raise GST and other fees, especially at current difficult times. Government finance is sometimes complicated and the ordinary person does not understand this is not public money to be spent on them. I have kicked this dead horse several times, but I would like to share yet another primer, this time with simple graphics.

As usual, such an event is followed by public outcry why with so much reserves, the government is reluctant to increase social spending and instead raise GST and other fees, especially at current difficult times. Government finance is sometimes complicated and the ordinary person does not understand this is not public money to be spent on them. I have kicked this dead horse several times, but I would like to share yet another primer, this time with simple graphics.

Fig.1 MAS buys foreign currency/sells S$

MAS manages the S$ exchange rates by setting a band within which it is allowed to move for each pair of currency. If there is an upward pressure on the S$ say for the S$/US$ pair, MAS intervenes in the FX market to sell S$ and buy US$. MAS pays for the US$ simply by crediting the reserve account of the counterparty bank with the S$. The counterparty bank transfers US$ to MAS account at the Federal Reserve in New York.

The MAS thus increases its foreign currency inventory (Official Foreign Reserve) with nothing. It simply credits a bank's account. This is commonly referred to as "printing" money. So technically, MAS has unlimited power to buy foreign currencies. Some people tend to see this as "money is for free".

On the other hand, to buy S$, MAS has to pay for it with real foreign currencies. MAS intervenes in the FX market to buy S$ when there is downward pressure on the local currency. Thus MAS needs to maintain a certain level of Official Foreign Reserves at all times.

The MAS thus increases its foreign currency inventory (Official Foreign Reserve) with nothing. It simply credits a bank's account. This is commonly referred to as "printing" money. So technically, MAS has unlimited power to buy foreign currencies. Some people tend to see this as "money is for free".

On the other hand, to buy S$, MAS has to pay for it with real foreign currencies. MAS intervenes in the FX market to buy S$ when there is downward pressure on the local currency. Thus MAS needs to maintain a certain level of Official Foreign Reserves at all times.

Fig.2 Inflationary effect of 'printing' S$

Once the S$ is with the bank, it gets circulated into the market which increases the supply of money. Money gets deposited with banks and banks lend them out. Bank A lends to customer A who deposits at Bank B. Bank B lends to customer B who deposits at Bank C, and so on. This is called fractional banking and it has a multiplier effect on the supply of money. How much the money can multiply depends on the reserve requirements set by MAS. The reserve requirement means banks cannot lend out the full amount deposited with them. They need to keep a certain sum with MAS. If the reserve requirement is 10%, the S$1,000 can end up with S$10,000 through fractional banking.

Thus the 'printing' of S$ by MAS has a downside. Too much money supply creates inflationary pressure on goods and services. One of the key responsibilities of MAS is to ensure price stability. That means it has to find a way to negate the expansion of money supply when it purchases foreign currencies in its market intervention.

Thus the 'printing' of S$ by MAS has a downside. Too much money supply creates inflationary pressure on goods and services. One of the key responsibilities of MAS is to ensure price stability. That means it has to find a way to negate the expansion of money supply when it purchases foreign currencies in its market intervention.

Fig.3 Sterilising the S$ 'printed' in market intervention

To remove from the market the S$ that was 'printed' to pay for the foreign currency, the central bank issues MAS Bills. These are S$ denominated short term securities of 4 to 12 weeks. Investors buy these MAS Bills and pay through their banks which essentially means MAS debits the banks' accounts. The liability is recorded as a credit in the MAS Bills account. The S$1,000 is thus removed from the market, or sterilised.

The effect in the books is MAS has changed its liability from due to banks to a debt instrument, ie MAS Bills. In other words, the foreign currencies are actually funded by debt.

The effect in the books is MAS has changed its liability from due to banks to a debt instrument, ie MAS Bills. In other words, the foreign currencies are actually funded by debt.

Fig.4 Transfer of excess OFR to government

MAS determines when to transfer excess OFR to the government. The Ministry of Finance issues RMGS (Reserves Management Government Securities) which are subscribed by MAS. RMGS are non-tradeable securities denominated in S$. They are issued solely as a mechanism for MAS to transfer excess OFR to the government.

MAS transfers the US$ to the bank in New York where GIC has their account. In MAS books, the asset has now changed from Foreign currency to Securities - RMGS. (There are other internal entries to deal with the dual currency transaction).

The excess OFR ends up with GIC to invest. In this example, GIC co-mingles the original OFR sum of US$1,000 into their investment portfolio. The currency risk is managed by GIC. What is important to note here is that the asset (investment) is carried in the books of GIC, but the ultimate liability, the MAS Bills, is in MAS books.

To put it bluntly, the GIC investments represented by this US$1,000 is not public money. The S$75 billion OFR transferred out of MAS into GIC is not for the goverment to spend.

MAS transfers the US$ to the bank in New York where GIC has their account. In MAS books, the asset has now changed from Foreign currency to Securities - RMGS. (There are other internal entries to deal with the dual currency transaction).

The excess OFR ends up with GIC to invest. In this example, GIC co-mingles the original OFR sum of US$1,000 into their investment portfolio. The currency risk is managed by GIC. What is important to note here is that the asset (investment) is carried in the books of GIC, but the ultimate liability, the MAS Bills, is in MAS books.

To put it bluntly, the GIC investments represented by this US$1,000 is not public money. The S$75 billion OFR transferred out of MAS into GIC is not for the goverment to spend.

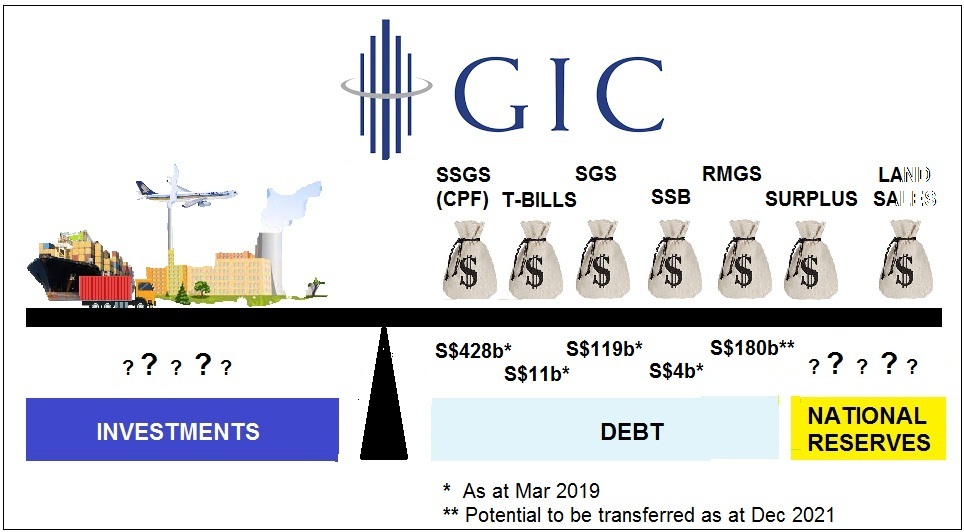

Fig.5 Reserves and National Reserves

Reserves are sums of money that are set aside for specific purposes. These reserves include debt (various government securities) and national reserves (from accumulated budget surpluses, government land sales, and the original equities transferred to Temasek at its formation), This distinction is necessary because only the national reserves portion belong to the people of Singapore collectively.

How the national reserves can be spent is regulated by law. This prevents any political party, on winning the mandate to govern, to pursue frivolous fiscal policies.

The reserves from debt instruments cannot be spent. By law, money raised from the issuance of the various government securities cannot be spent. Those securities are not issued for fiscal purposes but for other specific objectives, eg SSGS and RMGS is for transferring CPF money and MAS excess OFR to GIC to invest

Closing words:

The S$75b transferred from MAS to GIC this month is not money the government can spend on Singaporeans. There is a debt on the liabilities side of MAS books to repay. Growth in the foreign reserves in MAS is not profits. Let's not criticise the government for not using this S$75B to help alleviate the people's problems.

How the national reserves can be spent is regulated by law. This prevents any political party, on winning the mandate to govern, to pursue frivolous fiscal policies.

The reserves from debt instruments cannot be spent. By law, money raised from the issuance of the various government securities cannot be spent. Those securities are not issued for fiscal purposes but for other specific objectives, eg SSGS and RMGS is for transferring CPF money and MAS excess OFR to GIC to invest

Closing words:

The S$75b transferred from MAS to GIC this month is not money the government can spend on Singaporeans. There is a debt on the liabilities side of MAS books to repay. Growth in the foreign reserves in MAS is not profits. Let's not criticise the government for not using this S$75B to help alleviate the people's problems.

5 comments:

If the money cannot be spent, if it cannot be touched, why the need to transfer? If it is to be invested, why can't it be invested in the Singapore people?

@ Sharon

Thank you for visiting.

MAS maintains the foreign currencies as reserves for monetary policy management purposes. It can be 'touched' whilst in MAS. It is used to buy back S$ when the exchange rate drops to the lower band so as to push the rates up again. That is the purpose of holding foreign currency reserves -- to protect the S$.

Whilst these foreign currencies are with MAS, they are invested. But MAS being a central bank, cannot invest in longer term and higher risk/higher return assets.

Thus MAS transfers to GIC to invest. GIC's portfolios can make better returns. Of course that makes sense. At least that is the official view. I have my other views on this matter which I will expand in a coming blog.

What I meant the government cannot spend on the people is there is a liability side to these money. It is the MAS Bills that MAS owes to investors who indirectly funded MAS purchase of the foreign currencies. These foreign reserves are not profits that the government can spend.

Investing on the people is fiscal spending, which by law the government cannot do for the proceeds of several types of government securities, including the RMGS in regards to the transfer of MAS foreign reserves.

Great piece, very well explained!

Just commenting on the "public outcry" line, re "so much reserves".

Much has to do with the Government's insistence in not revealing the "true" national reserves.

Have a look at the MOF FAQ page:

https://www.mof.gov.sg/policies/reserves/what-comprises-the-reserves-and-who-manages-them

As an accountant, I'm quite happy to read the opening Summary:

"The reserves refer to the total assets minus liabilities of the Government and other entities specified in the Fifth Schedule under the Constitution1."

But go to Q6 and you'll see this:

"MAS and Temasek publish the size of the funds they manage. As of 31 March 2021, the Official Foreign Reserves managed by MAS was S$510 billion and the size of Temasek’s net portfolio value was S$381 billion.

It is the size of the Government’s funds managed by GIC that is not published. What has been revealed is that GIC manages well over US$100 billion. Revealing the exact size of assets that GIC manages will, taken together with the published assets of MAS and Temasek, amount to publishing the full size of Singapore’s financial reserves."

Q6 "redefines" reserves as gross assets or some variation of it, totally disregarding liabilities which upsets the accounting balance in me. By a strict definition, reserves of MAS @ 31 Mar 2021 is net assets = $47.495B. Similarly, Temasek is credited with Net Portfolio Value of $381B whilst the Group Balance Sheet @ 31 Mar 2021 show Shareholder Equity of $347B.

Official financial statements tend to irk people like me, e.g. Government Financial Statements are scant in details and prepared on a cash basis! Another whole story can be unfolded there …

Given the current state of official disclosures, I can well understand the "public outcry" whenever the word reserves is mentioned.

Sources:

https://www.mas.gov.sg/-/media/MAS-Media-Library/publications/annual-report/2021/MAS-Financial-Statement-2021.pdf

https://www.temasekreview.com.sg/group-financials/group-balance-sheets.html

https://www.parliament.gov.sg/docs/default-source/default-document-library/cmd-10of2021.pdf

@ Loh Kin Poh

Thank you. With your background, you know where I'm coming from. It's good to be understood.

That's the MOF explainer opening summary you referred :

"The reserves refer to the total assets minus liabilities of the Government and other entities specified in the Fifth Schedule under the Constitution1."

Yes, and I explained this in July 2021 in my blog :

Tiktok video brags Singapore grew richer by more than S$200B during pandemic. It's hogwash and here's why. ( https://chem-post.blogspot.com/2021/07/Singapore-reserves-grew-pandemic-S200b.html ).

Regarding Q6.

"Revealing the exact size of assets that GIC manages will, taken together with the published assets of MAS and Temasek, amount to publishing the full size of Singapore’s financial reserves"

A couple of qualifications:

- Statutory boards and the myriad of of entities held by them have are not included in government accounts. To get a full and complete picture, these have to be included. No idea what their net assets are.

- The Q&A makes the same mistake as most people in referring to the Official Foreign Reserves as reserves. To the extent that some of these foreign liquid assets are acquired by debt (sterilised market intervention, use of Government deposit balances from proceeds of govt securities), they are not reserves.

- To the extent that Temasek has gone into the debt market to take advantage of cheap money, and investing on leveraged basis, much like private equity funds, the aggregate portfolio do not represent our reserves.

Yes, cash accounting does make it very difficult to see the big picture. We can't fault them on this. Public accounting and fund accounting are all done this way. It does serve their purpose.

Good post that one in July 2021 - bean counters they like to poke fun of accountants but the ingrained concept of double entry is an extremely useful tool to see both sides of the coin ... :)

Just to add some of my findings from too much time on hand as a semi-retired bean counter:

1. Stat Boards - last count I did was for FY 31 Mar 2020 based on published audited accounts

Gross NAV = $550B

Less CPFB = $428B

Est Net NAV (all others) = $122B

Excluded are the unavailable numbers from DSTA (no publicly audited accounts for same reason as no breakdown for MINDEF in Budget Revenue Estimates)

2. Previously Stat Boards now University Companies by Guarantee

NAV FY 31 Mar 2020 = $23B

3. MOH Holdings Pte Ltd, an oft-forgotten company owning SingHealth

4. others? SPH Media (akan datang?)

Government Financial Statements (GFS)

Cash Accounting has to go, many 3rd world countries have already transited to accrual accounting:

https://www.ifac.org/knowledge-gateway/supporting-international-standards/discussion/international-public-sector-financial-accountability-index-2020

https://www.ifac.org/system/files/publications/files/IFAC-CIPFA-International-Public-Sector-Accountability-Index.pdf

The GFS is actually fascinating reading - most commentators are fixated on the Balance Sheet, that 1 page that is published together with each Annual Budget Statement. Read the accounts notes and they'll find nuggets ...

Post a Comment