The video was obviously inspired by an article posted by Critical Spectator (CS). It is a mindless steal of someone's idea rehashed into another medium, without the faintest idea of the subject matter.

CS is a controversial Singapore-based foreigner who writes profusely and largely supportive of Singapore government policies. Outside of local issues, I actually find his articles quite interesting. On Jul 14 CS wrote unabashedly on how Singapore's reserves rose by more than S$200b during the pandemic. He referred to the increase of S$160b in the Official Foreign Reserves (OFR) of Monetary Authority of Singapore from 2019 to 2021, and the S$75b profits Temasek made for 2021. According to him, our reserves increased by S$235b.

Following a rebuttal by Facebook contributor Chris Kuan, CR responded with basically a 2019 speech by MAS's Ravi Menon explaining how Singapore manages its reserves. But CS got it wrong again.

What is national reserve :

How much is our national wealth or reserves is a trillion dollar question. Both Kenneth Jeyeratnam and Prof Balding (HK-based academic) have written extensively on this and suggested the reserves are well over a trillion S$. It is far in excess of what's managed by MAS, Temasek, and estimated GIC numbers. The duo compute based on some macro data approach which I do not comprehend. They have persistently asked where are the missing billions!

We need first to understand what is national reserves. Some have tried to incorporate the idea of latent wealth -- the untapped oil and mineral reserves underground, the forestry, etc. Quantifying these is problematic. Fortunately, or unfortunately for us, Singapore has none of these. It is easier to talk of our national wealth.

The government is the steward of the economy, so it should have some book-keeping done. Imagine the government has a huge ledger and is able to produce one single consolidated balance sheet for all its activities, just like any commercial enterprise. The national wealth can be derived in the way a company's net worth is appraised.

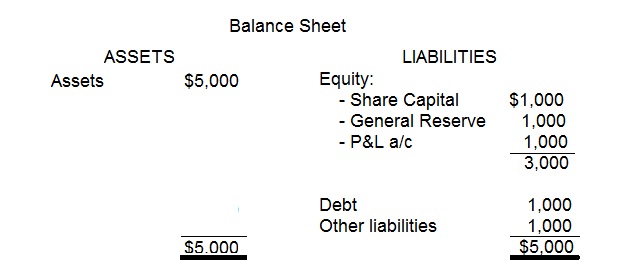

A quick book-keeping lesson here.

In very basic terms, a balance sheet will look like this. The P&L a/c represents the net of all the Expenses and Revenue accounts. At the end of the year, assuming there is no distribution, the net profit is finalised and transferred to the General Reserve which will then be S$2,000. The net worth of the enterprise is the Total assets $5,000 - Liabilities $2,000 = Net asset S$3,000, which is = Equity.

The net asset, which is also Equity, is what an enterprise is worth. An increase in the net asset figure represents an increase in the value of the enterprise.

Thus a giant government balance sheet will have a net asset figure which represents our national wealth. CS is saying during the pandemic, this net asset figure has gone up by at least S$235b. As he put it, it could be more because he did not include GIC.

By definition, our national reserve is the aggregate of the net assets of all the ministries, all statutory boards and Fifth Schedule companies. MAS, GIC, Temasek, CPF, HDB, and JTC comprise the Fifth Schedule companies. The statutory boards comprise of 65 entities. View here.

Now that we understand national reserves, what are past reserves and why is the distinction important. Past reserves refer to the increase in the net assets generated by previous governments. The use of past reserves is protected by Law.

Someone once famously quipped it will take a few hundred years to list down all the national assets. But taking the net asset view, I posit it is certainly possible to compute the aggregate reserves of the state within one day.

How are our reserves managed :

The reserves are managed by MAS, Temasek and GIC. In other words, be clear that the portfolios managed by these 3 entities are not our total national reserve. As described above, the national reserve is the sum total of the net assets of all the ministries, stat boards and Fifth Schedule companies. The portfolios managed represent funds taken out of those entities and funneled into the fund managers. In other words, our real national reserves are much more than the portfolio numbers of these 3 entities.

So how does reserves get funneled to the 3 fund managers.

1. Government surpluses are transferred to Treasury.

2. Proceeds from government land sales (HDB/JTC?) are transferred to Treasury.

Treasury channels (1) and (2) to GIC to invest. Occasionally, the government transfers some funds to Temasek.

3. Of the net profits of MAS, 17% are distributed to govt Consolidated Funds, balance 83% the MAS transfers to its General Reserve Fund which it manages.

4. For GIC and Temasek, a special long term risk-factored formula is applied on the portfolio to arrive at what is known as the NIRC (net investment returns contribution). This portion of the net profits is distributed back to the government to help fund the budget. The balance of the profits is ploughed back as capital.

What about CPF ? By law, our pension money can only be invested with the government. For this purpose, the government securitise the debt by issuance of SSGS (special Singapore govt securities). This guarantees CPF a fixed return in a risk free security. The SSGS also serves a very important function of price discovery for the S$ yield curve. Proceeds of the SSGS, ie our CPF money, is funneled to the GIC to invest and seek better yields. Point to note, which are most often misunderstood by the majority. The government does not make use of our CPF money. It is invested by GIC. Of course, if GIC generates a better ROI than the interest on SSGS, the benefits do not trickle down to CPF members. But that's another story.

So can we have an idea of how our reserves are performing, or at least that part that is being managed by MAS, GIC and Temasek? With MAS, it is not possible because all their investments are co-mingled. You can't tell which belongs to the national reserves. With GIC there are 2 problems. The portfolio is from co-mingled funds of reserves and CPF money. And of course, it is impossible because GIC data is secret. With Temasek, it is possible since the whole portfolio is from reserves. But it can be done only to the extent the data permits. Temasek is not that transparent.

The claim of S$235b increase in wealth is hogwash :

With the primer on national reserves out of the way, we can now review the claim intelligently.

Error #1 :

It is incorrect to assert an increase of national reserves solely on the figures of MAS and Temasek as these are not exhaustive. There are so many other state entities for which the data is unknown.

Error #2 :

Error #3:

Like most layman, CS mistook the foreign exchange reserve in MAS books as reserves. They are very liquid foreign assets. These are assets set aside for some purpose, that's why they are commonly referred to as foreign exchange reserves. All central banks maintain such a reserve for the purpose of supporting at least 6 months of the country's importation of goods. They are also required for the central banks to manage their currency floats, that is, to stabilise their currency exchange rate. MAS maintains a very high level of these assets. In fact our foreign exchange reserves is one of the highest in the world. The reason why MAS maintains such a high foreign exchange reserve recognises Singapore as an international financial centre which needs substantial foreign currency liquidity in the local market. A high reserve makes for a very strong S$.

The foreign reserve assets increased by S$122.077b from 2019 to 2021 (S$519.128b-S$407,051) I have no idea where CS obtained his S$160b. An increase on the asset side is reflected in an increase in the liabilities side somewhere. That is, the foreign asset increase has to be funded from somewhere. This can be seen in increases in money printing (S$10b), increase in banks reserve deposits (S$12b) MAS securities issued (S$35.5b), other liabilities- repos (S$81b). This increase in foreign assets has nothing to do with our national reserves. Neither does it represent greater wealth for the country.

Did Temasek perform that well:

I don't intend to discuss Temasek's performance in 2021 here but only to clarify the claim of the S$75b profits in 2021 and to raise some issues. Instead of making the bold claim of huge profits, I think questions ought to be raised.

Error #4 :

The claim was our reserves went up by S$235b during the pandemic of which S$160b is from MAS (2019-2021) and Temasek S$75b (2021). In order to refer to the same period, Temasek's figure should also be for 2 years 2019-2021.

The increase in Temasek net assets or equity over the 2 years is S$347.5b-S$283.5b = S$64b. The claim that Temasek increased the national reserves by its profit of S$75b is wrong.

Error # 5:

CS referred to a net profit of S$75b by Temasek in 2021. That is not correct. The net profit was only S$56.5b. Perhaps he rounded it up to S$57b and made a typo transpositional error to S$75b?

The issues with the net profit of S$56.5b :

The S$56.5b profit for 2021 was an impressive 24.53% return on shareholder funds. The return is a more realistic 16.4% on the average portfolio of S$343.5b ((opening S$306b + closing S$381b) /2). This points to either high leverage, or due to high shareholder fund enhancement over the years. More work is needed to look into this.

Of course as an investment company,asset valuation impact its P&L. During the year, the Singapore Stock Exchange was lethargic, moving up only 8.7%. Dow Jones Industrial Average , however, climbed a whopping 65% during the year. 20% of the portfolio was in US. Of the 27% portfolio in China, most of these were listed in US. And so too with some of the Indian counters. So a big chunk of the profits was due to the fact the year started on a very low valuation.

A significant impact on the profit was IFRS9. Under IFRS9, changes in the mark-to-market valuation of listed companies in which Temasek hold less than 20% control are now brought into the group P&L. This is the international accounting standard that Temasek adopted and which came into effect in 2019. In 2019 and 2020 these holdings showed a small valuation loss. In 2021, the valuation profit was S$45.5b thus contributing to 81% of the profit. Without this, the profit would have been only S$11b, representing a mere 4.8% ROI on shareholder fund and 3% against average portfolio. And this against the backdrop of a 65% climb at Dow Jones.

Another question is how did this under sub-20% holdings valuation gains came about in 2021? This can only happen in 3 ways :

(1) It had a large holding of sub-20% listed companies. Suppose they are all US counters where the stocks gained 65%, then this holdings must be at least S$72b to generate the S$46.5b valuation gains.

(2) It made huge new investments of sub-20% stocks at the earlier part of the year when prices were generally lower.

(3) It disposed of huge inventory sub-20% stocks which had been carrying substantial valuation loss provisions. Upon disposal, the negative counters disappear from the exercise, pushing valuation into positive territory.

However, (1) cannot be discerned with no data. (2) and (3) are unlikely as divestment was only S$49b and new investments S$39b. Too small to be causation for the S$46.5b valuation gains.

Read "Temasek profits is wool over eyes"Another old issue I want to bring up again. Temasek Review shows only group earnings. It would be nice to have a sense of how much profits were generated by Temasek itself. You can read my old blog above.

Read "Is Temasek operating a slush fund?"

With good profits come good bonuses. But we will never know how much, it's national secret. Run and compensated like private equity funds, you can bet it's in millions. Read my old blog above.

Conclusion :

The tiktok video with false info will go viral. This informative blog will just circulate amongst my few friends. That's symptomatic of today's reality. The truth for the day is, Singapore did'nt grow richer by S$235b during the pandemic.

3 comments:

I have to respond to it here for proper perspective - a synopsis of our exchange on Facebook.

You've made the same mistake that Chris Kuan did - you're looking at it too narrowly, merely adding up positions on the balance sheet without understanding what they mean.

There is a reason that reported figures for every central bank in the world show not the net assets of the bank but the official foreign reserves of the country - and why those with relatively high reserves are looking for ways to invest the money that has poured into the local economy from abroad.

So, let's answer the simple question first - did Singapore get richer by S$160bn through rapid accumulation of Official Foreign Reserves in the last year?

YES, there is no doubt about that - and the reason there is no doubt about it is the fact that OFR are a component of Net International Investment Position, which is, de facto, an element in the process of estimating the country's overall net worth.

NIIP itself essentially shows the difference between the country's foreign assets and the assets other countries have in the country.

I.e. how much Singapore as a whole owns abroad vs. what abroad owns in Singapore.

This figure is updated quarterly and reported for the entire economy - and it has, actually, grown by S$350 billion since the start of the pandemic.

What it means, simply put, is that if all residents of Singapore (individuals, companies and government) wanted to liquidate their foreign assets and pay off the liabilities (what foreign countries own in SG), the country would walk away with close to S$1.4 trillion in surplus vs. S$1.05 trillion at the end of 2019.

OFR form a part of this figure and, as such, have contributed to the country getting, de facto, richer.

Looking at the balance sheet of MAS is not going to tell you that, because foreign reserves are matched on the opposite side by domestic liabilities. As they should be, since the size of OFR is simply a measure of excess demand for SGD, that is backing the current exchange of the dollar.

As foreign investors flock to Singapore - as one of financial safe havens - the demand for SGD grows and so MAS has to intervene in the market to keep its exchange rates low. I.e. it sells more SGD and acquires more currencies.

MAS reported currency interventions in 2020, to the tune of an equivalent of nearly US$100bn - what matches the figures.

But it cannot allow the excess SGD it exchanged for USD and other currencies to be sloshing around the market, because it would create enormous excess liquidity in the Singapore Dollar.

To absorb it, it issues bills that banks purchase for SGD - and which end up on MAS' balance sheet as domestic liabilities.

It follows a simple patter: high demand for SGD -> intervention -> bill issuance to sterilize it.

As a result, Singapore owns more without owing more (and its domestic liabilities to not matter for this calculation, since they are settled within the boundaries of one economy - i.e. merely changing pockets in the country).

There's no other way of defining it than as "getting richer".

Now, a valid question could be - what can be done with this money?

Because getting richer through OFR doesn't necessarily mean the funds can be spent. After all - they are backing the currency that may suddenly need intervention in the opposite direction.

The fact is, however, that Singapore's OFR are so high that a good portion can be invested in less liquid assets to yield higher profits - and for that purpose funds are occasionally moved to GIC (like they were in 2019, when S$45bn where move to the corporation for investing).

I.e. then while the funds may not necessarily be spent and most of them can only be held in highly liquid, but not very profitable, financial assets, a good portion of them can be treated as funds that can be put in e.g. foreign equities.

In fact, this is how GIC itself was born - through huge OFR surpluses that were moved for profitable management outside of the central bank.

As for the Errors you alleged:

#1 - Nowhere did I make such an assessment. I did mention that GIC figures are incoming and are likely to be very good too.

Typically, and officially, these three large pools are treated as national reserves. Balances of other Fifth Schedule companies are inconsequential. CPF is exchanging its funds for special bonds proceeds from which go to GIC already. And HDB has to be regularly subsidized.

Hence, the only three you have to look at are MAS, GIC and Temasek.

(This does not include nonfinancial assets like land etc. because calculating that would be downright impossible. But yeah - SG has even more wealth, just not particularly liquid, so it's pointless to mention it here. That said = proceeds from land sales do end up in one of the three pots anyway - so when the land sales are realized and are countable, they are included too.)

#2 - Net assets of the central bank, as I explained, are not the relevant figure here.

#3 - I explained how OFR make Singapore richer through NIIP. MAS effectively prints more SGD - which it can do without any downside when demand is high - and acquires valuable USD.

#4 - Incorrect. I measured end of 2019 to June of 2021 for MAS (by its reports). And March 2020 to March 2021 for Temasek (as its reported there). It's the closest we have to estimate the impact of the pandemic - which is what my article was about.

#5 - Again, you're mistaking profit for shareholder return. I'm interested in the value of the portfolio, little else. It went up from S$306 to S$381 billion - S$75 billion since March 2020.

PS. If you want to bring up high DJIA returns do everyone a favor and bring up DJIA losses compared to Temasek's reported results last year. The role of the company is not to act as an index fund but to invest money prudently and safely, while also supporting a number of important SG based companies.

Michael

Appreciate your comments here.

I'm no economist, but I do understand what you are saying whilst you on the other hand do not appreciate what I said.

I don not wish to get into a discussion on the Balance of Payments side of things and trade and capital flows that end up with OFR. It's simply too laborious.

You were mixing up the NIIP with our national reserves. Higher NIIP thus Singapore gets richer. As you well know the NIIP reflects Singapore's position with the rest of the world. That is a world of difference with national reserves.

National reserves are by definition the government's, aka the public, aka the citizens' of Singapore. The national reserves, as I mentioned, comprise of all the unencumbered assets of the ministries, statutory boards and the Fifth Schedule companies. All these belong to the public. If these go up, yes, it represents we are richer. And these asset could be domestic or foreign.

On the reverse side, the national debt represents what the government owns, which ultimately is a public liability. Eg the US national debt is now US$28.5T. It is the Federal debt owed to Americans and foreigners, which means each American man, women and child owes about US$92,000.

The NIIP represents one country's claim vs the rest of the world. If Singapore has a positive NIIP it means we have more claims against other countries. If there is an increase in NIIP does that mean we are richer? The answer is a flat NO. Simply because NIIP is a way of looking at a country's position. It does not reflect a public position. The foreign wealth of the billionaires of Singapore - the Kweks, the Ongs, the Ngs and what have you, the thousands of foreign enterprises and MMCs, are their private wealth, they do not belong to Singapore citizens, they are not national reserves.

Back in the 1600s, had there been similar data, the NIIP of India never represented wealth of the Indians. It all belonged to the English East India Company.

As I explained, our government cleverly funneled the institutions surpluses into the 3 entities that invest the funds. If the portfolio values of these funds go up, of course they have increased wealth. But why did I say it is wrong to look at national wealth increase based on these 3 portfolios alone. Because, as I mentioned, our national institutions comprise of close to 100 entities. What if one of these entities had a disastrous year? We were never know of the actual status unless we have full data.

Post a Comment